Insurance Partners

United Family Healthcare accepts health insurance plans offered by most major insurance companies. Our insurance company directory is updated frequently, so if your insurance plan is not in the directory, please call us for a consultation.

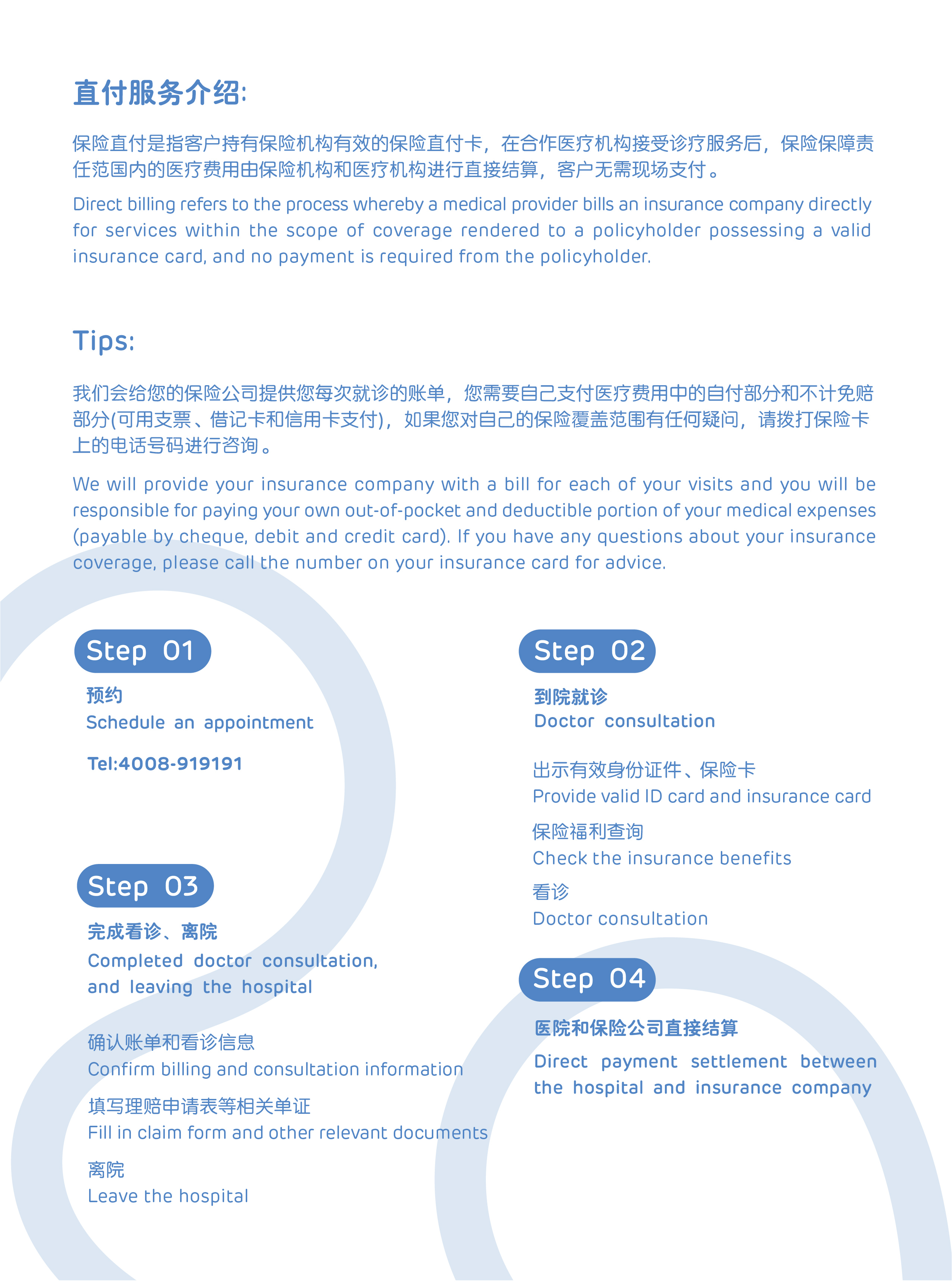

How do I use my insurance at United Family Healthcare?

We will provide your insurance company with a bill for each of your visits and you will be responsible for paying your own co-pay and deductible portion of your medical expenses, the same as if you had been seen at another clinic. The amount paid by your insurance company varies depending on the health insurance plan you have. If you have any questions about your insurance coverage, please call the number on your insurance card for advice. The out-of-pocket portion of medical expenses, as well as expenses that require cash payments, may be paid by debit and credit cards at.

Reminder: United Family Healthcare only offers direct billing to one insurance company per patient.

What if I don’t have insurance? No problem.

At United Family Healthcare, we believe that modern, quality care should be accessible to everyone, including patients without health insurance. Our simple fee structure takes the guesswork out of pricing medical services, so you can come in anytime and stay within your budget. Whether you need to see a doctor, get vaccinations or treat a medical condition, our fees are reasonable. To make it easier for you to pay for your visit, we accept debit and credit card payments at.

How can I find a health insurance plan that best suits my needs?

You’ll find a plethora of health insurance plans that exist online, but which one is best for you and your family or your employees?

For a United Family Hospital (UFH) patient, having a health insurance plan with which we have a direct billing relationship will make it easier for you. Today, Shenzhen New Frontier United Family Hospital has more than 20 insurance providers with varying degrees of direct billing, and more will be added. All of these insurance providers offer different insurance plans.

Some plans are designed for people who visit the doctor frequently and will cover a wide range of services, including annual physicals, gastroscopies, mammograms, genetic tests, prostate exams, vaccinations, oral services and maternity options, and more. Simpler insurance plans will focus more on basic medical protection or be specifically designed for emergency care and major medical conditions.

What should I look for when choosing health insurance?

Annual maximums amounts of claim should be noted: Annual claim limits under a health insurance plan can range from hundreds of thousands of RMB to millions of RMB. The higher, the better, as a day in the hospital in an emergency can cost tens of thousands of RMB. UFH recommends that your insurance claim limit should ideally be above RMB 5 million.

The Co-payment rate for High cost hospital visit should be note: insurance companies usually classify different types of medical facilities. Shenzhen New Frontier United Family Hospital has agreed with Cigna-CMB, GBG China, and AXATP to include hospitals on the non-expensive list. Please look for our subsequent updates on the list of partner insurers for non-expensive hospitals.

Pre-existing conditions should be noted: Typically, health insurance plans for individuals and small organizations do not pay benefits for pre-existing and regularly occurring conditions. However, some health insurance plans will cover certain pre-existing conditions. When you apply for this type of plan at, your insurance company may require a complete medical history to verify that your condition is covered by the insurance. As you can expect, these plans are about two to three times more expensive than plans that do not cover pre-existing conditions.

Be aware of emergency evacuation: Most medical insurance policies for foreigners residing in China will support emergency evacuation benefits. In the event of an emergency, if appropriate medical care is not available in your area, your insurance company will arrange and pay for transportation to the nearest appropriate hospital as soon as possible.

Attention should be paid to outpatient treatment matters: when you are only consulting with a doctor by appointment rather than being hospitalized, what you are receiving is an outpatient service. It may include a doctor’s consultation, laboratory tests, prescribed medications, and subsequent tests. If you have been to an outpatient clinic within the last year or two for a minor illness such as a headache or fever, it is important to consider whether outpatient treatment should be covered under your insurance plan.

Pregnancy period requirements should be noted: it is customary for large group insurance plans to cover the cost of pregnancy periods without requiring a so-called waiting period, as the insurer already has hundreds or thousands of group employee premiums on hand. However, for individuals or small companies, there is a waiting period required for pregnancy benefits. Therefore, if you are planning to have a child in the near future, planning ahead will save you tens of thousands of RMB. The average waiting period is 12 months, so check your insurance plan at to confirm.

Attention should be paid to annual medical examinations and periodic treatment: large group insurance plans usually cover annual medical examinations and periodic treatment services. Individual or small company insurance plans will also cover these services and may include a waiting period. Sometimes, mammograms, genetic tests, prostate exams, vaccinations and eye services are included in this category. Please contact your insurance company to confirm the requirements and terms.

Attention should be paid to the cost of dental treatment: depending on what is being treated, dental service options will have different benefit percentages. For example, many policies will cover an exam and x-rays, oral cleanings once or twice a year, 80% of the cost of fillings and root canals, 50% of the cost of bridges and crown fillings, and so on. Of course, each insurance plan will have different provisions and it is recommended that you contact your insurance company and check the relevant provisions in your own insurance plan.